The Bank of Canada today held its target for the overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%.

The war in the Middle East has increased volatility in global energy prices and financial markets, and heightened the risks to the global economy. The breadth and duration of the conflict, and hence its economic impacts, are highly uncertain.

Prior to the war, the global economy was on pace to grow at around 3%, as expected in the January Monetary Policy Report (MPR). Economic growth in the United States has moderated but remains solid, driven by consumption and strong AI-related investment. US inflation remains above target and has evolved largely as expected. In the euro area, domestic demand is supporting growth while exports have contracted. China’s economy continues to be boosted by strength in exports, but domestic demand remains weak.

Since the outbreak of the conflict in the Middle East, global oil and natural gas prices have risen sharply, and this will boost global inflation in the near-term. In addition to energy supply disruptions, transportation bottlenecks stemming from the effective closure of the Strait of Hormuz could impact the supply of other commodities, such as fertilizer. Financial conditions have tightened from accommodative levels. Global bond yields have risen, equity market prices have declined, and credit spreads have widened. The Canada-US dollar exchange rate has remained relatively stable.

After expanding by 2.4% in the third quarter of last year, GDP in Canada contracted 0.6% in the fourth quarter. This was weaker than expected at the time of the January MPR, but mainly because of a larger-than-expected drawdown in inventories. Domestic demand grew by more than 2% due to strength in consumer and government spending, even as housing markets remained weak.

We continue to expect the Canadian economy to grow modestly as it adjusts to US tariffs and trade policy uncertainty, but recent data suggest that near-term economic growth will be weaker than anticipated in January. The labour market remains soft. Employment gains in the fourth quarter of 2025 were largely reversed in the first two months of 2026, and the unemployment rate rose to 6.7% in February. Looking through the volatility, recent data also suggest ongoing weakness in exports. It’s too early to assess the impact of the conflict in the Middle East on growth in Canada.

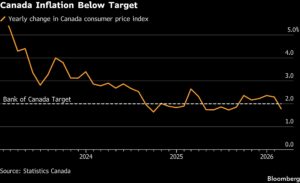

CPI inflation eased further to 1.8% in February, down from 2.3% in January. CPI inflation excluding changes in indirect taxes as well as core inflation measures have also come down and are all close to 2%. Food inflation slowed in February but remains elevated. The sharp increase in global energy prices has led to increases in gasoline prices, and this will push up total inflation in the coming months.

Against this overall backdrop, Governing Council decided to maintain the policy rate at 2.25%. With recent data pointing to weaker economic activity and uncertainty elevated, risks to growth look tilted to the downside. At the same time, inflation risks have gone up due to higher energy prices. We will continue to assess the impact of US tariffs and trade policy uncertainty, and how the Canadian economy is adjusting. We are also monitoring the unfolding conflict in the Middle East closely and assessing its impact on growth and inflation. As the outlook evolves, we stand ready to respond as needed. The Bank is committed to ensuring that Canadians continue to have confidence in price stability through this period of global upheaval.

Information note

The next scheduled date for announcing the overnight rate target is April 29, 2026. The Bank’s next MPR will be released at the same time.

This article is reposted from the Bank of Canada website.