Spring mortgage season is bringing better fixed-rate deals, but not all borrowers are seeing relief. While lenders continue trimming fixed rates, discounts on variable rates are shrinking.

If you’re in the market for a mortgage this spring, you’ve probably noticed fixed rates are continuing to trend lower.

That’s thanks in large part to falling bond yields, which drive fixed-rate pricing, and a fresh wave of spring competition among lenders.

“The spring market starts now,” mortgage analyst Ron Butler recently toldCanadian Mortgage Trends, pointing to what’s typically the busiest—and most competitive—season in the mortgage cycle. With many high-ratio fixed rates now dipping below 4% for the first time in months, Butler says the pricing war is well underway.

According to rate expert Ryan Sims, big banks are especially keen to compete right now after a sluggish start to the year for mortgage originations. That’s translating into sharper fixed-rate offers across the board.

While the Bank of Canada’s overnight rate dropped another 25 basis points earlier this month, lenders are quietly reducing their variable-rate discounts off prime—effectively making new variable-rate mortgages more expensive.

It’s a trend that hasn’t gone unnoticed by brokers and borrowers alike.

As more borrowers eye variable products in anticipation of future BoC rate cuts—as reflected in the latest big bank rate forecasts—lenders are adjusting pricing, but not for the usual reasons.

While fixed mortgage rates tend to move with bond yields, variable rates are tied to the Bank of Canada’s overnight rate. However, the discounts lenders offer off their prime rate can shrink when credit spreads widen—that is, when the cost of borrowing for lenders increases relative to government bond yields.

This means that even as bond yields fall, lenders may reduce variable-rate discounts to preserve their profit margins in the face of rising credit costs.

EconoScope:

Upcoming key economic releases to watch

Country

Date

Time (ET)

Release

Previous reading

Wed

March 26

1:30 p.m.

BoC Summary of Deliberations

Wed.

March 26

8:30 a.m.

Durable Goods Orders (February)

+3.1% MoM

$282.3B

Thurs.

March 27

8:30 a.m.

Survey of Employment, Payrolls and Hours (January)

+25.3k (+0.1%)

Thurs.

March 27

8:30 a.m.

Initial Jobless Claims (Mar 22)

Thurs.

March 27

8:30 a.m.

Real GDP (Q4, third estimate)

+2.3%

Thurs.

March 27

8:30 a.m.

Advance Economic Indicators Report (February)

Thurs. March 27

10:00 a.m.

Pending Home Sales (February)

-4.6%

Fri.

March 28

8:30 a.m.

Monthly Real GDP (January)

+0.2%

Fri.

March 28

Ottawa’s Fiscal Monitor for January (expected)

Fri.

March 28

8:30 a.m.

Personal Income & Consumption (February)

Income: +0.9%

Fri.

March 28

10:00 a.m.

University of Michigan Consumer Sentiment Index (March final)

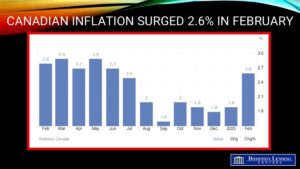

Canadian Inflation surged to 2.6% in February, much stronger than expected.

The Consumer Price Index (CPI) rose 2.6% year-over-year (y/y) in February, following an increase of 1.9% in January. With the federal tax break ending on February 15, the GST and HST were reapplied to eligible products. This put upward pressure on consumer prices for those items, as taxes paid by consumers are included in the CPI.

While the second straight acceleration in the headline number was expected, the pace of price gains may still surprise Bank of Canada policymakers, who cut interest rates for the seventh straight meeting. Donald Trump’s tariff threats hamper business and consumer spending. But assuming the federal sales tax break hadn’t been in place, Canadian inflation would have jumped even higher to 3% in February. This is at the upper bound of the bank’s target range, from 2.7% a month earlier. Canadian inflation has not been at or above 3% since the end of 2023.

Faster price growth was broad-based in February, the end of the goods and services tax (GST)/harmonized sales tax (HST) break through the month contributed notable upward pressure to prices for eligible products. Slower growth for gasoline prices (+5.1%) moderated the all-items CPI acceleration.

The CPI rose 1.1% m/m in February and 0.7% on a seasonally adjusted basis. However, the increase exceeded the tax impact as seasonally-adjusted CPI excluding the tax impact was +0.4%. And, in case you want to pin it on food & energy, CPI excluding food, energy & taxes was +0.3%.

Gains were across the board, with the sectors impacted by the tax change seeing the most significant increase: recreation +3.4%, food +1.9%, clothing +1.6%, and alcohol +1.5% more to come next month, with the tax holiday only ending in mid-February. The headline inflation figures are subject to as much noise as we’ve seen in decades. They are poised to continue for at least another couple of months, making it very challenging to interpret the inflation data.

As a result, prices for food purchased from restaurants declined at a slower pace year over year in February (-1.4%) compared with January (-5.1%). Restaurant food prices contributed the most to the acceleration in the all-items CPI in February.

Similarly, on a yearly basis, alcoholic beverages purchased from stores declined 1.4% in February, following a 3.6% decline in January.

On a year-over-year basis, gasoline prices decelerated, with a 5.1% increase in February following an 8.6% gain in January. Prices rose less month over month in February 2025 compared with February 2024, when higher global crude oil prices pushed up gasoline prices, leading to slower year-over-year price growth in February 2025. Month over month, gasoline prices rose 0.6% in February. This increase was primarily related to higher refining costs amid planned refinery maintenance across North America. This offset lower crude oil prices, mainly due to increased American supply and tariff threats, contributing to slowing global growth concerns.

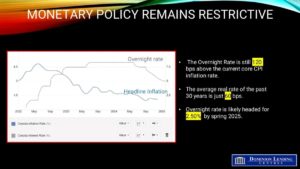

One notable exception to the broad-based strength was shelter, rising “just” 0.2%. That’s the smallest gain in five months, trimming the yearly pace to 4.2%, the slowest since 2021, with more downside to come. Mortgage interest costs rose a modest 0.2% for a second straight month, slicing it to +9% y/y, ending a 2½-year run of double-digit increases.

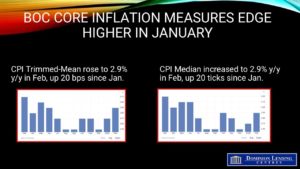

Not surprisingly, the core inflation metrics were firm as well. CPI-Trim and Median both rose 0.3% m/m and 2.9% y/y. The 3- and 6-month annualized rates are all above 3% as well, pointing to ongoing stickiness. The breadth of inflation, which has been a focus for the Bank of Canada, also worsened with the share of items rising 3%+ increasing modestly. None of this is encouraging news for policymakers.

Bottom Line

This report will reinforce the Bank of Canada’s cautious stance on easing to mitigate the impact of tariffs. Notably, the upcoming end of the carbon tax will cause inflation to drop sharply in April. However, March may see an increase in inflation as the effects of the tax holiday begin to reverse. There is still a lot of uncertainty surrounding inflation, which complicates the job of policymakers. We will see what April 2 brings regarding additional tariffs.

If the economic outlook did not worsen, the Bank of Canada might consider pausing after cutting rates at seven consecutive meetings. However, the Canadian economy will likely slow significantly in the coming months.

Bank of Canada Governor Tiff Macklem said last week the bank would “proceed carefully”amid the tariff war. Economists are still awaiting more clarity on tariffs before firming up their expectations for the next rate decision on April 16, when policymakers will also update their forecasts. Right now, traders are betting that the BoC will hold rates steady in April, but a lot can and will happen before then.

US president vows massive retaliation to Ontario energy tariffs, repeats annexation threats

Donald Trump’s trade war continued to roil financial markets on Tuesday as the US president announced he was doubling tariffs on Canadian steel and aluminum and vowed massive further retaliation against Canada for Ontario’s electricity surcharge.

The S&P 500 slid to a six-month low as Trump ramped up his rhetoric while the Dow Jones also tumbled and five-year Government of Canada bond yields, which lead Canadian fixed mortgage rates, slipped on Tuesday morning before posting a slight recovery.

Five-year yields were perched just above 2.6% at time of writing, having slumped since the end of February when Trump’s tariffs loomed into view again after an initial 30-day pause.

The president took to Truth Social on Tuesday morning to respond to Ontario’s new 25% levy on electricity to the US and said Canada would pay “a financial price for this so big that it will be read about in History Books for many years to come.”

He said he had instructed commerce secretary Howard Lutnick to slap additional tariffs on Canadian steel and aluminum, bringing those charges to 50%, and once again floated the idea of the US annexing Canada.

“The only thing that makes sense is for Canada to become our cherished Fifty First State,” Trump wrote. “This would make all Tariffs, and everything else, totally disappear.”

Karoline Leavitt, the White House press secretary, said Canada would face “grave consequences” if Ontario shut off power to the US, while Trump vowed to declare a national emergency on electricity within the regions impacted by the surcharge.

The extra charges on steel and aluminum, which are set to take effect on Wednesday morning, could ramp up home prices south of the border, with Trump having already targeted Canadian softwood lumber for heavy tariffs.

They mark a new escalation in a trade war, launched last week by Trump, that has sent financial markets into a tailspin and raised the prospect of big rate reductions for both fixed and variable mortgages in Canada.

The Bank of Canada is scheduled to make its second rate decision of the year tomorrow, with a 25-basis-point cut widely expected – and further cuts could be on the way if the trade crisis continues.

Mark Carney, who won the Liberal Party’s leadership race to succeed Justin Trudeau and will be sworn in as prime minister in the coming days, has confirmed his government will keep Canada’s countermeasures against US tariffs in place “until the Americans show us respect and make credible, reliable commitments to free and fair trade.”

Ontario premier Doug Ford said on Tuesday afternoon he would temporarily lift the electricity surcharge and is expected to meet with Lutnick later this week to discuss the trade dispute further.

President Donald Trump has officially confirmed that tariffs on Canadian and Mexican imports will go into effect on March 4, 2025, following his comments earlier this week suggesting a delay.

Trump plans to impose a 25% tariff on imports from Mexico and Canada, while applying a reduced 10% tax on Canadian energy products, including oil and electricity.

In a post on Truth Social, Trump said the decision was driven by ongoing concerns over “unacceptable levels” of drugs entering the U.S. from both countries, with a specific focus on fentanyl flowing through the borders.

“We cannot allow this scourge to continue to harm the USA, and therefore, until it stops, or is seriously limited, the proposed TARIFFS scheduled to go into effect on MARCH FOURTH will, indeed, go into effect, as scheduled,” Trump wrote. “China will likewise be charged an additional 10% Tariff on that date.”

Bank of Canada Governor Tiff Macklem recently warned of the economic fallout Canada could face if the trade conflict intensifies.

“Increased trade friction with the United States is a new reality,” he said, cautioning that such a shock wouldn’t be temporary—it would fundamentally alter Canada’s economic trajectory,” Macklem said.

“The economic consequences of a protracted trade conflict would be severe,” he continued. “If tariffs are long-lasting and broad-based, there won’t be a bounce-back. We may eventually regain our current rate of growth, but the level of output would be permanently lower.”

On Thursday, Mexican President Claudia Sheinbaum expressed optimism, stating that Mexico remains hopeful it can negotiate a deal with the U.S. to avoid the looming tariffs, despite the recent announcement.

Markets are bracing for the impact, as analysts predict that these tariffs could lead to higher costs for U.S. consumers, putting additional strain on the broader economy. This move is expected to heighten market volatility, as traders and analysts weigh the potential ripple effects on global supply chains.

Analysts are watching closely as these moves could signal broader trade tensions, with Trump hinting at further 25% tariffs on the European Union as well.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

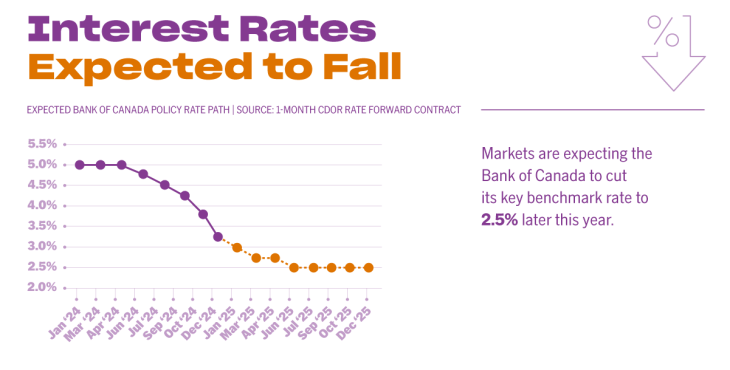

Variable mortgage rates are looking increasingly attractive compared to fixed rates, with the potential for significant savings, according to new research from BMO Economics.

With additional Bank of Canada rate cuts expected this year, the bank argues that variable-rate mortgages could offer borrowers more savings over the long run.

“With borrowing costs more likely to fall than rise—and by a lot in a possible trade war—a floating rate mortgage could pay off,” writes senior BMO economist Sal Guatieri.

While current variable mortgage rates are roughly on par with—or slightly higher than—5-year fixed rates, Guatieri notes they’re “unlikely to stay there.”

How variable rates are priced

Unlike fixed mortgage rates, which are influenced by bond yields, variable rates are tied to lenders’ prime lending rates.

These, in turn, follow the Bank of Canada’s overnight policy rate, which currently sits at 3.00%. The current prime rate offered by major lenders is 5.20%, meaning most variable rates are currently priced at a discount off the prime rate.

Most economists expect the Bank of Canada to continue cutting rates this year, in addition to the six consecutive rate cuts the Bank delivered last year. That means lenders’ prime rates should follow suit—bringing down borrowing costs for variable-rate mortgage holders.

Where rates are headed

BMO’s latest forecast sees the Bank of Canada’s policy rate falling to 2.50% by later this year, or potentially down to 1.50% in the event of a full-fledged trade war with the U.S. (See full story here). Under the base-case scenario, this would likely push the prime rate below 4.50%, meaning today’s variable-rate borrowers could see meaningful savings.

Other big banks generally share this outlook, with CIBC, National Bank, and TD all expecting the BoC policy rate to drop to 2.25% by year-end, while RBC is even more aggressive, forecasting a fall to 2.00%.

BoC policy rate forecasts from the Big 6 banks

Current Policy Rate:

Policy Rate:

Q1 ’25

Policy Rate:

Q2 ’25

Policy Rate:

Q3 ’25

Policy Rate: Q4 ’25

Policy Rate: Q4 ’26

BMO

3.00%

3.00%

2.75%

2.50%

2.50%*

2.50%

CIBC

3.00%

2.75%

2.25%

2.25%

2.25%

2.25%

NATIONAL BANK

3.00%

2.75%

2.50%

2.25%

2.25%

2.75%

RBC

3.00%

2.75%

2.25%

2.00%

2.00%

SCOTIABANK

3.00%

2.75%

2.75%

2.75%

2.75%

2.75%

TD

3.00%

2.75% (-25bps)

2.25% (-50bps)

2.25% (-25bps)

2.25%

2.25%

* Assumes no U.S. tariffs. Expected policy rate of 1.50% in the event of tariffs. Updated: February 24, 2025

More borrowers are turning to variable rates

Courtesy: Edge Realty Analytics

With variable rates looking more appealing, more borrowers are already reconsidering their mortgage options.

Data from the Bank of Canada shows that as of November, nearly a quarter of new mortgages were variable-rate—up from less than 10% earlier in the year.

Mortgage broker Ron Butler told Canadian Mortgage Trends previously that this trend has only accelerated in recent months, noting that the share of variable mortgages he’s originating has jumped from 7% last year to 40% today.

Why BMO thinks it’s a smart bet

BMO argues that with rate cuts ahead, borrowers choosing variable rates today are positioning themselves for lower payments in the near future.

“We estimate a borrower putting 10% down on a half-million-dollar home financed over 25 years would save an average of 40 bps per year compared with locking in for five years,” he wrote. “That equates to just over $100 per month or more than $6,000 in five years.”

In the event that a trade war with the U.S. “torpedoes the economy,” Guatieri says the savings could be even greater, with variable-rate borrowers saving an additional 29 bps on average over the 5-year term—or an extra $74 per month.”

Another benefit, Guatieri notes, is that that variable-rate borrowers still have the flexibility to lock in if rates unexpectedly start to rise.

While there’s always a degree of uncertainty, Guatieri believes the bigger risk is locking into a fixed rate and missing out on potential savings.

Weighing the risks and alternatives

While BMO’s forecast aligns with market expectations for 50 bps in rate cuts this year, Guatieri acknowledges that there’s no guarantee the Bank of Canada will ease further.

“Should the Bank stand pat on rates, locking in could pay off moderately,” he wrote. “Furthermore, the economy could strengthen materially if a trade war is averted, causing inflation to reheat and the Bank to unwind some rate cuts. In this case, a fixed rate would clearly be the better choice.”

For risk-averse borrowers, a shorter-term fixed rate could be a middle ground.

Three-year fixed rates are currently slightly lower than five-year rates and provide the flexibility to refinance sooner at a potentially lower variable rate. According to BMO, this approach could save borrowers about 20 bps per year over five years compared to locking in for the full five years today.

“While that’s still 20 bps higher than opting for a variable rate today, the extra cost may be worth paying to hedge against potential rate increases,” Guatieri added.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

Canada’s inflation report for January has led to a sharp decline in the chances of the Bank of Canada cutting rates in March.

Canada’s headline inflation rate rose by 1.9% year-over-year in January, a slight increase from December’s 1.8% and in line with expectations.

The increase in headline CPI was largely driven by higher energy prices, notably gasoline (+8.6%) and natural gas (+4.8%).

The Goods and Services Tax (GST) holiday, which ran from mid-December to mid-February, provided some relief. This temporary measure helped reduce prices for food purchased at restaurants (-5.1% y/y), alcoholic beverages (-3.6% y/y), and toys, games, and hobby supplies (-6.8% y/y).

Core inflation measures, which are closely monitored by the Bank of Canada, showed a more mixed picture. CPI excluding food and energy remained stable at 2.2% y/y, but the seasonally adjusted annualized rate of CPI excluding food and energy slowed to 1.6% in January from 4% in December.

However, the Bank of Canada’s preferred core inflation measures, CPI-Trim and CPI-Median, both edged higher to 2.7% y/y, signalling that underlying inflation pressures remain. Moreover, the three-month annualized trend of core inflation has been tracking above 3%, suggesting that core inflation “could continue to rise in the coming months “should continue to grind higher,” noted TD economist James Orlando.

Impact on Bank of Canada rate cut expectations

Following today’s release, market odds of a 25-basis-point rate cut at the Bank of Canada’s March 12 policy meeting dropped to under 30%.

“There is too much underlying inflationary pressure in Canada to warrant an inflation-targeting central bank easing monetary policy further,” wroteScotiabank‘s Derek Holt.

“The state of the job market also does not merit further easing,” he added, referencing January’s higher-than-expected job growth. “Canadian inflation remains too warm for the Bank of Canada to continue easing.”

However, economists remain divided on the Bank of Canada’s next move. Some, like Oxford Economics, still expect the Bank to continue cutting rates in the months ahead.

“The Bank of Canada will be in a bind as it weighs competing concerns over higher prices from the tariffs with the drag on economic growth,” noted Tony Stillo, Director of Canada Economics at Oxford.

“We believe the BoC will look through the temporary price shock and instead focus on the negative implications for the Canadian economy and heightened trade policy uncertainty, leaving it on track to lower the policy rate another 75bps to 2.25% by June 2025,” he added.

TD’s Orlando also underscored the challenge the Bank of Canada faces in balancing competing priorities.

“Does it weigh the downside risks to the economy in the face of U.S. tariffs, or does it focus on recent economic strength and the impact this is having on inflation?” he questioned, while acknowledging that much can change between now and the next BoC policy meeting.

“There is plenty of time between now and March 12, and if the President’s first few weeks are anything to go by, a lot could change before then,” he added.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

After the Bank of Canada’s latest rate reduction 5-year variable mortgage rates are now on par with their fixed-rate counterparts, raising the question: Is now the time to go variable?

With additional Bank of Canada rate cuts expected, variable-rate mortgages are becoming an increasingly attractive option.

But choosing flexibility comes with its challenges—borrowers must weigh potential savings against heightened market volatility and the growing uncertainty surrounding a possible trade war with the U.S.

Ron Butler of Butler Mortgages told Canadian Mortgage Trends that this is the most volatile time he’s seen in the bond market “in forever.”

“It’s literally like 2008, during the Global Financial Crisis, it’s so wild,” he said.

Butler notes that the Canadian 5-year bond yield, which typically leads fixed-mortgage rate pricing, fell from a high of 3.85% in April to 2.64% last week, a significant change in such a short period of time. As a result, following six consecutive Bank of Canada rate cuts, 5-year variable rates are now nearly on par with fixed equivalents.

Clients opting for variable rates in droves

Look past the volatility—and the threat of devastating U.S. tariffs —and variable rates present a compelling case.

Markets are still pricing in at least two more quarter-point Bank of Canada cuts this year, which could push variable mortgage rates down at least another 50 basis points.

Some forecast even more aggressive rate-cut action will be required to counter the ecnoomic shock of a trade war with the U.S.

“I don’t think it’s a stretch to believe that the Bank will reduce its policy rate from its current level of 3.00% down to at least 2% during the current rate cycle,” David Larock of Integrated Mortgage Planners said in a recent blog.

However, he cautions that there is also the risk that rate hikes come back into play should inflationary pressures re-emerge.

“While I expect variable rates to outperform today’s fixed-rate options, I caution anyone choosing a 5-year variable rate today to do so only if they are prepared for a rate rise at some point over their term,” Larock added. “Five years is long enough for the next rate cycle to begin, and for variable rates to rise from wherever they bottom out over the near term.”

Still, it’s a risk more and more borrowers are willing to take. Data from the Bank of Canada shows that as of November, nearly a quarter of new mortgages were variable-rate, up from less than 10% earlier in the year.

Butler says this trend has only accelerated in recent months, noting that the share of variable mortgages he’s originating has surged from 7% last year to 40% now.

“We advise clients to take variable because we now have actual reporting from marketplace analysts that it will go down,” he says. “The fee benefit of variable is a guaranteed penalty amount; you just don’t know what penalty you’re really going to get with fixed.”

Unlike fixed-rate mortgages, which often come with interest rate differential (IRD) penalties that can amount to tens of thousands of dollars, variable-rate mortgages typically carry a much smaller penalty—just three months’ interest—making them a more flexible option for borrowers who may need to break their mortgage early.

Butler argues that if tariffs are imposed, their impact on the mortgage market won’t be immediate, as inflation would primarily rise due to retaliatory counter-tariffs. This lag, he says, could give variable-rate borrowers a window to switch to a fixed rate before higher inflation forces the Bank of Canada to reverse course and hike rates.

“This kind of trade war means that in the beginning, the economy deteriorates, and interest rates go down; it takes nine months or a year for the inflation to really lock into a point where the Bank has to raise rates,” he says. “The inflation spiral takes time. The Bank of Canada will cut long before costs start to increase.”

Tracy Valko of Valko Financial, however, suggests that in such a trade war inflation becomes secondary to more immediate economic indicators, like unemployment. That, she warns, could skyrocket following a tariff announcement as companies brace for impact.

“‘Inflation’ was the word last year; this year I think it will be ‘employment,’ because tariffs will drive unemployment, and people won’t be able to afford housing, which will put a lot of pressure on the government infrastructure,” she says. “I don’t think it will be like inflation, which is a lagging indicator, because businesses will have to adjust quite quickly, and we could see massive unemployment in certain sectors.”

Even Trump’s latest tariff threat on aluminum and steel imports could have devastating impacts on Canadian workers in those industries within days.

Valko adds that high unemployment would potentially drive interest rates down faster—potentially even triggering an emergency rate cut, as National Bank had suggested—to blunt the effects of high tariffs. That potential scenario, Valko says, adds to the variable rate argument, but also adds to the widespread feeling of uncertainty in the market.

“A lot of people are really pessimistic right now on the future; we’ve had clients and homeowners that have had a lot of shocks in the mortgage market and the real estate market, and are not interested in having any more instability,” she says. “People are more educated than they’ve ever been before, so they are really looking at their financing—which is great to see—but people are very cautious, so to take variable, it has to be a very risk-tolerant client.”

Rate options for the more risk-averse borrowers

Valko notes that borrowers wary of economic uncertainty are increasingly choosing shorter-term fixed rates, offering stability without locking in for the long haul.

“Three-year fixed has been probably the most popular because it’s not taking that higher rate for the traditional five-year fixed rate term,” she says. “They’re hoping in three years we’ll see a more normalized and balanced market.”

For more cautious borrowers, hybrid mortgages—which split the loan between fixed and variable rates—are another option and are currently available through most major financial institutions.

“There are some people that are in the middle of that risk tolerance, and if they could put a portion in fixed and a portion in variable—and to be able to adjust it quickly—I think it would be a really good option,” Valko says.

Butler, however, disagrees.

“A hybrid mortgage means you are always half wrong about mortgage rates,” he says. “If the balance of probability clearly indicates variable is the correct short-term answer, take variable and carefully monitor the movement of fixed rates.”

Jared Lindzon is a freelance journalist and public speaker based in Toronto. He is a regular contributor to the Globe & Mail, Fast Company and TIME Magazine, and has been published in The New York Times, Rolling Stone, The Guardian, Fortune Magazine, and many more.

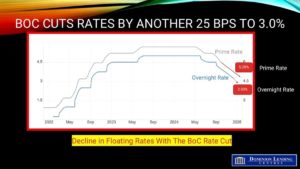

The Bank of Canada (BoC) reduced the overnight rate by 25 basis points this morning, bringing the policy rate down to 3.0%. The market had anticipated a nearly 98% chance of this 25 basis point reduction, and consensus aligned with this expectation. The Federal Reserve is also set to announce its rate decision this afternoon, where it is widely expected to maintain the current policy rate. As a result, the gap between the US Federal Funds rate and the BoC’s overnight rate has widened to 150 basis points. This discrepancy is largely attributed to stronger growth and inflation in the US compared to Canada. Consequently, Canada’s relatively low interest rates have negatively impacted the Canadian dollar, which has fallen to 69.2 cents against the US dollar. Additionally, oil prices have dropped by five dollars, now at US$73.61.

The Bank also announced its plan to conclude the normalization of its balance sheet by ending quantitative tightening. It will restart asset purchases in early March, beginning gradually to stabilize and modestly grow its balance sheet in alignment with economic growth.

The projections in the January Monetary Policy Report (MPR) released today are marked by more-than-usual uncertainty due to the rapidly evolving policy landscape, particularly the potential threat of trade tariffs from the new administration in the United States. Given the unpredictable scope and duration of a possible trade conflict, this MPR provides a baseline forecast without accounting for new tariffs.

According to the MPR projections, the global economy is expected to grow by about 3% over the next two years. Growth in the United States has been revised upward, mainly due to stronger consumption. However, growth in the euro area is likely to remain subdued as the region faces competitiveness challenges. In China, recent policy actions are expected to boost demand and support near-term growth, although structural challenges persist. Since October, financial conditions have diverged across countries, with US bond yields rising due to strong growth and persistent inflation, while yields in Canada have decreased slightly.

The BoC press release states, “In Canada, past cuts to interest rates have begun to stimulate the economy. The recent increase in both consumption and housing activity is expected to continue. However, business investment remains lackluster. The outlook for exports is improving, supported by new export capacity for oil and gas.

Canada’s labor market remains soft, with the unemployment rate at 6.7% in December. Job growth has strengthened in recent months after a prolonged period of stagnation in the labor force. Wage pressures, previously sticky, are showing some signs of easing.

The Bank forecasts GDP growth to strengthen in 2025. However, with slower population growth due to reduced immigration targets, both GDP and potential growth will be more moderate than previously anticipated in October. Following a growth rate of 1.3% in 2024, the Bank now projects GDP to grow by 1.8% in both 2025 and 2026, slightly exceeding potential growth. As a result, excess supply in the economy is expected to be gradually absorbed over the projection horizon.

CPI inflation remains close to the 2% target, though with some volatility stemming from the temporary suspension of the GST/HST on select consumer products. Shelter price inflation remains elevated but is gradually easing, as anticipated. A broad range of indicators, including surveys on inflation expectations and the distribution of price changes among CPI components, suggests that underlying inflation is near the 2% target. The Bank forecasts that CPI inflation will remain around this target over the next two years.

Aside from the potential US tariffs, the risks surrounding the outlook appear reasonably balanced. However, as noted in the MPR, a prolonged trade conflict would most likely result in weaker GDP growth and increased prices in Canada.

With inflation around 2% and the economy in a state of excess supply, the Governing Council has decided to further reduce the policy rate by 25 basis points to 3%. This marks a substantial (200 bps) cumulative reduction in the policy rate since last June. Lower interest rates are expected to boost household spending, and the outlook published today suggests that the economy will gradually strengthen while inflation remains close to the target. Nevertheless, significant and widespread tariffs could challenge the resilience of Canada’s economy. The Bank will closely monitor developments and assess their implications for economic activity, inflation, and monetary policy in Canada. The Bank is committed to maintaining price stability for Canadians.Nevertheless, significant and widespread tariffs could challenge the resilience of Canada’s economy. The Bank will closely monitor developments and assess their implications for economic activity, inflation, and monetary policy in Canada. The Bank is committed to maintaining price stability for Canadians.

Bottom Line

The central bank dropped its guidance on further adjustments to borrowing costs as US President Donald Trump’s tariff threat clouded the outlook.

Bonds surged as the market absorbed the central bank’s decision not to guide future rate moves. The yield on Canada’s two-year notes slid some four basis points to 2.79%, the lowest since 2022. The loonie maintained the day’s losses against the US dollar.

In prepared remarks, Macklem said while “monetary policy has worked to restore price stability,” a broad-based trade conflict would “badly hurt” economic activity but that the higher cost of goods “will put direct upward pressure on inflation.”

“With a single instrument — our policy rate — we can’t lean against weaker output and higher inflation at the same time,” Macklem said, adding the central bank would need to “carefully assess” the downward pressure on inflation and weigh that against the upward pressure on inflation from “higher input prices and supply chain disruptions.”

In the accompanying monetary policy report, the central bank lowered its forecast for economic growth in 2025 due to the federal government’s lower immigration targets. The bank expects the economy to expand by 1.8% in 2025 and 2026, down from 2.1 and 2.3% in previous projections. The central bank trimmed business investment and exports estimates but boosted its consumption forecast.

The bank estimated that interest rate divergence with the Federal Reserve was responsible for about 1% of the depreciation in the Canadian dollar since October.

We expect the BoC to continue cutting the policy rate in 25-bps increments until it reaches 2.5% this Spring, triggering continued strengthening in the Canadian housing market.

The federal government’s launch of the Secondary Suite Refinance Program on January 15 was largely met with optimism, but some brokers note that questions remain.

The program, first unveiled in October, allows homeowners to refinance up to 90% of their property’s value (capped at $2 million) to build secondary suites intended for long-term rental use, specifically excluding short-term rentals like Airbnb.

In a previous post, Canadian Mortgage Trends examined the pros and cons of the program, concluding that it appears to offer significant benefits for homeowners looking to boost their investments or ease financial pressures by adding a tenant. The initiative also holds potential to create jobs and contribute to the broader housing supply.

However, the program’s details remain unclear, creating uncertainty that has made some brokers hesitant to fully support homeowners seeking to refinance.

“It’s very bare bones,” says Connor Green, a mortgage agent with Concierge Mortgage Group, referring to the limited information and criteria available for the program so far. “Typically with a product of this nature you’d see something much more fleshed out.”

There has also been limited information available to homeowners eager to take advantage of the program, particularly regarding the application process.

The Canada Mortgage and Housing Corporation (CMHC), which is overseeing the program, told Canadian Mortgage Trends, “Interested homeowners should reach out to their lender or mortgage provider.”

Overall details of who will qualify remain vague

Since the program’s January 15 launch, key details remain unclear, including financing logistics, timelines, permit and zoning requirements, and inspection criteria, critics say.

“I think there needs to be more direction on how the funds are going to be managed,” notes Tracy Valko, Principal Mortgage Broker and Founder of Valko Financial. “They’re saying it’s a refinance, but typically with a refinance you give funds on closing … we know that won’t be the case with this but then there needs to be some rollout about what that expectation is.”

Young happy couple examining blueprints during home renovation process in the apartment.

Even the program’s very definition of a “distinct secondary suite” remains unclear.

With the core incentive open to interpretation, homeowners face uncertainty when deciding on specific development options, such as a basement suite, laneway house, garden suite, or a simple partition within the home. Each option carries the risk of not aligning with potential future clarifications provided by the government, critics say.

“‘Distinct secondary suite’ is very vague,” notes Green. “Is that an addition? A detached unit? A basement apartment? Is it splitting a basement apartment into two units, three units? … It’s all vague in that sense where I’m not exactly sure what they are looking to finance under this program.”

Opportunity for multi-generational home owners unclear

One demographic that appears to have been overlooked in the initial planning and follow-up information for the program is homeowners seeking to refinance for the creation of multi-generational homes—households that accommodate at least three generations of the same family.

A 2021 Statistics Canada report revealed a sharp rise in multi-generational homes over the past two decades, with their numbers increasing by 50% between 2001 and 2021.

Such homes would also benefit from support to expand but are more likely to focus on projects that accommodate additional family members rather than tenants, such as creating in-law suites or undertaking “non-distinct” expansions.

However, since the federal government’s new Secondary Suites Refinancing Program is specifically geared towards the creation of rental units, it seems, at least for now, to overlook the opportunity to offer refinancing options for this rapidly growing demographic of homeowners.

Looming tariffs add to the uncertainty

Another source of uncertainty is the looming U.S. tariffs, which could drive up the cost of labour and materials needed for renovations under the program.

Shortly after being sworn in on January 20, U.S. President Donald Trump announced plans to impose a 25% tariff on goods imported from Canada, set to begin February 1. While the tariffs might not directly impact renovation projects in Canada, the potential for retaliatory measures and an escalating trade war could disrupt supply chains and increase costs.

“Materials are expensive, labour is expensive in Canada now,” says Valko. “And there’s also the timeline—you don’t want to have a unit half completed and not be able to finish it by the end of the year … I think that’s why lenders are reluctant.”

Dylan Freeman-Grist is a freelance journalist based in Toronto covering a variety of topics including finance, art, design and technology. You can follow him on X or Bluesky @freemangrist.

The Canadian Housing Market Ends 2024 On a Weak Note

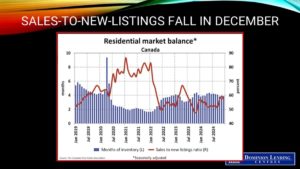

Home sales activity recorded over Canadian MLS® Systems softened in December, falling 5.8% compared to November. However, they were still 13% above their level in May, just before the Bank of Canada began cutting interest rates.

The fourth quarter of 2024 saw sales up 10% from the third quarter and stood among the more muscular quarters for activity in the last 20 years, not accounting for the pandemic.

“The number of homes sold across Canada declined in December compared to a stronger October and November, although that was likely more of a supply story than a demand story,” said Shaun Cathcart, CREA’s Senior Economist. “Our forecast continues to be for a significant unleashing of demand in the spring of 2025, with the expected bottom for interest rates coinciding with sellers listing properties in big numbers once the snow melts.”

New Listings

New listings dipped 1.7% month-over-month in December, marking three straight monthly declines following a jump in new supply last September.

“While housing market activity may take a breather over the winter with fewer properties for sale, the fall market rebound serves as a good preview of what could happen this spring,” said James Mabey, CREA Chair. “Spring in real estate always comes earlier than both sellers and buyers anticipate. The outlook is for buyers to start coming off the sidelines in big numbers in just a few months from now.”

With sales down by more than new listings on a month-over-month basis in December, the national sales-to-new listings ratio eased back to 56.9%, down from a 17-month high of 59.3% in November. The long-term average for the national sales-to-new listings ratio is 55%, with readings between 45% and 65% generally consistent with balanced housing market conditions.

There were 128,000 properties listed for sale on all Canadian MLS® Systems at the end of 2024, up 7.8% from a year earlier but still below the long-term average of around 150,000 listings.

There were 3.9 months of inventory on a national basis at the end of 2024, up from a 15-month low of 3.6 months at the end of November but still well below the long-term average of five months of inventory. Based on one standard deviation above and below that long-term average, a seller’s market would be below 3.6 months and a buyer’s market would be above 6.5 months. That means the current balance of supply and demand nationally is still close to seller’s market territory.

Home Prices

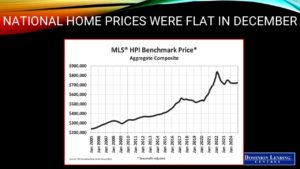

The National Composite MLS® Home Price Index (HPI) rose 0.3% from November to December 2024 – the second straight month-over-month increase.

The non-seasonally adjusted National Composite MLS® HPI stood just 0.2% below December 2023, the smallest decline since prices dipped into negative year-over-year territory last April.

The non-seasonally adjusted national average home price was $676,640 in December 2024, up 2.5% from December 2023.

Bottom Line

The Bank of Canada’s aggressive rate-cutting and regulatory changes that make housing more affordable have ignited the Canadian housing market. While the conflagration isn’t likely to peak until spring, a seasonally strong period for housing, activity already started to pick up in the fourth quarter.

Today, we saw a welcome dip in US inflation in December. Softer core US CPI inflation in December will give the Fed some breathing room ahead of the uncertain impact of tariffs. With the coming inauguration of Donald Trump, there is an inordinate amount of uncertainty. If Trump imposed tariffs on Canada in the early days of his administration, the Canadian economy would slow markedly, and inflation would mount. This could curtail the Bank of Canada’s easing and even trigger a tightening monetary policy if inflation rises too much.

Market-driven interest rates have risen sharply in recent weeks, pushing the interest rate on 5-year Government of Canada bonds upward. US ten-year yields are at 4.67%, up considerably since early December. Canadian ten-year yields have risen as well, but at 3.44%, they are more than 120 basis points below the US, well outside historical norms.

The central bank meets again on January 29 and will likely cut the overnight policy rate by 25 bps to 3.0%. Canada’s homegrown political uncertainty muddies the waters. The Parliament is prorogued until March as the Liberals decide on a new leader. The subsequent election adds to the volatility and uncertainty. We hold to the view that overnight rates will fall to 2.5% by midyear, triggering a strong Spring selling season.