People hunting for homes and mortgages have had a lot of economic and market news coming their way lately. Probably the most significant is the Bank of Canada’s decision to lower its policy rate.

As expected, the central bank trimmed a quarter of a point off its trendsetting interest rate, bring it to 2.50%. It is the first rate move since March.

The cut came a day after Statistics Canada reported the inflation rate rose to 1.9% in August, up from 1.7% in July.

Normally rising inflation would be a reason for the Bank not to lower its rate, due to concerns about over stimulating the economy and encouraging even more inflation. However, the Bank noted that other factors – such as stable (although higher than desired) core inflation, a decline in the gross domestic product and an increase in unemployment – indicate inflation is not a high risk.

The interest rate cut could make variable-rate mortgages look more attractive for those who are comfortable with potential rate movement.

The Canadian Real Estate Association reports August home sales increased 1.1% compared to July and were almost 2.0% better than a year earlier. The MLS Home Price Index showed flat pricing month-over-month, but registered a 3.4% decline year-over-year. CREA’s national average price was $664,000 in August 2025, up 1.8% from August 2024.

August new listings were up 2.6% over July and up 8.8% over a year earlier.

This article was published by the First National LLP Marketing Team on their website.

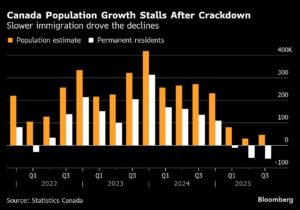

Once a runaway train, Canada’s immigration-driven population growth has come to a grinding halt.

By Randy Thanthong-Knight

(Bloomberg) — Once a runaway train, Canada’s immigration-driven population growth has come to a grinding halt.

For the second straight quarter, the country’s population changed nominally, compared with a quarterly growth rate of nearly 1% last year, according to Statistics Canada data released Wednesday.

Tighter immigration rules aimed at reducing the number of temporary immigrants drove almost more people out than new arrivals and natural births, with an increase of 47,098 people or 0.1% in the second quarter, the data showed. That’s a similar gain to the first three months of this year — and, except for 2020, the lowest growth rate in a second quarter since comparable records began in 1946.

The government’s plan to reduce the temporary migrant population appears to being working. The number of non-permanent residents dropped for the third time in a row, reaching 7.3% of the total population in the quarter, versus 7.6% at its peak. The decrease was driven by foreign students and workers leaving the country.

With half a year of essentially no population growth, Prime Minister Mark Carney’s government must decide whether to keep its tight lid on inflows or bring in more workers. The country’s new immigration targets are due Nov. 1.

It will be the first target set under Carney, who promised to bring immigration rates to “sustainable levels.” At the same time, his government wants to build homes and infrastructure to boost activity in a tariff-hit economy. That plan will require more skilled workers in trades and construction — sectors that still face labour shortages.

U.S. policies on immigration may also influence movements across the northern border, with some refugees as well as H-1B visa holders potentially heading to Canada.

In order to increase the number of intakes, Carney — who inherited eroded public support for mass immigration — will have to restore public confidence in the system and rebuild consensus around welcoming newcomers.

Like many of its advanced economy peers, Canada needs immigration to grow its population and tax base in order to replace workers and support its aging population. International migration accounted for more than 70% of population growth in Canada between April and June. In the second quarter, the number of births exceeded deaths by 13,404, with immigration adding 33,694 people.

Tepid population growth already clouded the economic outlook. Bank of Canada Governor Tiff Macklem said last week, when he resumed cutting interest rates, that low population growth as well as a weak labour market will weigh on household spending — a rare bright spot in the economy that contracted sharply last quarter.

National Bank of Canada’s top executive called on Prime Minister Mark Carney to consider bold tax cuts and deregulation for strategic sectors to boost the country’s productivity and competitiveness.

By Mathieu Dion

(Bloomberg) — National Bank of Canada’s top executive called on Prime Minister Mark Carney to consider bold tax cuts and deregulation for strategic sectors to boost the country’s productivity and competitiveness.

“We need to have lower taxes than the U.S. for businesses,” Chief Executive Officer Laurent Ferreira said at the Canada Fintech Forum in Montreal on Monday evening. The government should even think about a “zero tax policy” for strategic manufacturing and defense procurement, he said.

Ferreira, who has led Canada’s sixth-largest bank since 2021, told the audience the country’s productivity growth has been weak for a decade. “We need to wake up,” he said, also calling for fewer regulatory requirements in the manufacturing sector.

“We need to be more competitive. We have a hard time attracting capital. We have a hard time keeping our businesses in Canada.”

U.S. President Donald Trump’s tariff policies have sent a chill through Canada’s economy over the past several months. Gross domestic product contracted at a 1.6% annualized pace in the second quarter amid a drop in exports and soft business investment.

Most Canadian goods are still exempt from new U.S. levies under the U.S.-Mexico-Canada Agreement. But Trump’s tariff policy has shaken the automotive, steel and aluminum industries, and the unpredictable outcome of a new deal is leading many companies to wait before investing.

“No one really knows how tariffs are going to impact the U.S., Canada, and growing deficits around the world are also a big question mark for the bond market,” Ferreira said. “Those are obviously uncertainties that are around that and clients, businesses are on pause.”

Carney has promised to release a federal budget on Nov. 4 with substantial investments to boost the country’s economy. The government trimmed personal income taxes in July, but hasn’t indicated it’s considering large cuts to business taxes.

Canada faces significant budget pressures, partly because of increased military spending. The deficit will be about $70 billion this fiscal year, or more than 2% of GDP, according to the median estimate in a Bloomberg survey of economists.

Still, Ferreira praised the federal and provincial governments’ focus since the beginning of the trade war. “It’s an economic agenda, and it is very encouraging to hear everything that they’re working on,” he said about his discussions with government officials.

Oxford Economics says Canada’s economy will stay weak through 2025, with housing activity picking up but prices still expected to slide into 2026.

Oxford Economics expects Canada to remain on the edge of recession through 2026, warning that broad-based weakness across the economy shows little sign of easing.

The outlook was shared during the firm’s September Office Hours call, where economists pointed to persistent sluggishness across key sectors despite cooling inflation and recent rate cuts from the Bank of Canada.

Ongoing uncertainty around trade, a softening labour market and a housing market still searching for the bottom were flagged as key risks, with the path ahead also vulnerable to policy shocks such as the federal budget this fall.

Weak growth and a softening job market

Oxford Economics said the economy will “remain on the verge through the second half of 2025, teetering on recession,” with the Bank of Canada’s recent cut described as consistent with easing inflationary risks and faltering growth. Another reduction in October was noted as possible, though the outlook “is still subject to policy shocks,” including a fiscal boost anticipated in the federal budget this fall.

The firm now expects inflation to average 2.6% next year, down from earlier projections of 3%, while the labour market will continue to feel the strain. “We think there’s still a little bit of a hit coming to lift unemployment to 7.4%,” the call noted, though the rate should fall relatively quickly into 2026 as population growth slows.

The outlook pointed to a prolonged weak growth cycle. “Our outlook for the Canadian economy is not that optimistic — we expect to remain on the edge of recession into 2026, with overall growth close to zero,” Oxford said. Quarter-by-quarter gains are expected to come slowly, in the range of just one to three tenths of a percent.

Uncertainty over tariffs under USMCA was also cited as a risk. Until Canada secures a deal similar to those achieved by the UK or EU, the firm noted a cloud of uncertainty is expected to hang over tariff rates, dampening investment and related sectors.

Tentative housing rebound overshadowed by falling prices

Oxford Economics pointed to early signs of improvement in resale activity, noting “a pickup in sales and average prices in Toronto and Vancouver, and listings have also risen, so overall activity is starting to move a little bit.” However, benchmark prices — described as the stronger gauge — “have continued to drift lower.”

Further rate relief is expected to bring more buyers and sellers back into the market this fall, though the balance is likely to tilt toward a buyer’s market. “There will be a pickup in activity, but it will lead to prices drifting lower into 2026,” Oxford said.

Modest price growth could resume by 2027, but structural headwinds are expected to limit the upside. “Demographic shifts will limit overall housing demand, alongside ongoing affordability challenges, especially in the Greater Toronto and Greater Vancouver areas,” Oxford noted.

Over the longer term, home prices are expected to rise only slightly faster than inflation. “We anticipate a housing market rebalance in the late 2030s, but over the next five to 10 years house prices will be largely flat in real terms,” the firm said.

Government ambitions tempered by structural limits

On the construction side, Oxford Economics is projecting limited momentum in the near term. “The next couple of months and quarters are not looking particularly good,” the firm noted, with a relative uptick expected only by late 2026. Even then, the baseline is described as low, and any rebound would resemble a return to balance rather than a boom.

Government ambitions add another layer of complexity, with Ottawa’s recently announced Build Canada Homes program calling for a near doubling of housing output through modular and mass-timber construction. But Oxford warned such targets risk overshooting. “We think the government’s plan to double housing supply overdoes it. We see housing starts peaking near the 300,000-unit range in the latter half of the decade. With changing factors including aging boomers selling homes, for example, we could face an oversupply situation by the end of the decade if that government plan comes true.”

For now, the Canadian economy appears set to remain in a holding pattern — not fully in contraction, but still far from a clear path to recovery. With tariffs in flux, inflation expected to tick slightly higher in the long term, and housing still adjusting, the market is shaped more by uncertainty than conviction.

Steven is a finance writer with over four years of experience, working across several finance verticals. His writing has appeared on LowestRates.ca, Loans Canada, InTheKnow, Yahoo Finance and more. He holds an MA in World Literature from Maynooth University in Ireland, and currently resides in Vancouver, B.C.

Not all “first-time buyers” are created equal. Here’s how the rules differ across Canada’s most-used programs.

If you’ve been poking around the idea of buying your first home in Canada, you’ve probably noticed that “first-time homebuyer” doesn’t always mean what you think it does. Different programs, federal and provincial, define it in different ways, and that can make things confusing fast.

We work with a lot of clients who get tripped up by this. Someone will tell me they’re a first-time homebuyer because they’ve never bought a home in Canada, only to discover their previous home in another country disqualifies them from a key benefit here. Or, on the flip side, someone who owned a condo years ago doesn’t realize they might still qualify for certain first-time buyer programs again under the right circumstances.

So let’s break it down. Here’s how “first-time homebuyer” is defined across three major programs Canadians often rely on: the Ontario Land Transfer Tax Rebate, the RRSP Home Buyers’ Plan (HBP), and the First Home Savings Account (FHSA).

How does Ontario define a first-time homebuyer for the land transfer tax rebate?

If you’re buying property in Ontario, the land transfer tax (LTT) rebate is probably the first program you’ll hear about. It can save you up to $4,000 on the provincial land transfer tax, and another $4,475 on the Toronto municipal land transfer tax if you’re buying in the city.

But the eligibility rules here are strict.

The never-ever rule

To qualify:

You must be at least 18 years old

You must have never owned a home or any interest in a home anywhere in the world

You must live in the home as your principal residence within nine months of the purchase

And, here’s the kicker, your spouse or common-law partner must also never have owned a home while you’ve been together

That last point trips up a lot of couples. If your partner owned a home before you got together, you’re in the clear. But if either of you owned a property while in a relationship with the other, even if it was overseas, you’re disqualified.

I’ve had to deliver that disappointing news more than once. It’s a harsh line, but that’s the rule.

“The latest addition is that a purchaser must be either a Canadian Citizen or have Permanent Resident status.We had a file recently where spouses bought a house together- they are both first time homebuyers but she doesn’t have her PR yet so they got only half the rebate. Once she gets her papers she can apply for the rebate within 30 days of getting a confirmation of residency, very short window of opportunity.”

Maria went on to say she often hears comments like, “How would they know if I owned something back in X? The answer is all government agencies are inter-connected. Therefore, when they are applying for immigration and put in their application that they owned a home back home, it may trigger a re-assessment, together with penalties.”

How does the RRSP Home Buyers’ Plan define a first-time homebuyer?

The HBP is a popular option for buyers who want to tap into their RRSP savings, up to $60,000 per couple, to help with a down payment.

Thankfully, this program is more forgiving than the LTT rebate.

The four-year look-back rule

To qualify:

You must not have lived in a home that you (or your spouse/common-law partner) owned in the current year or the four preceding calendar years

You need a signed agreement to buy or build a qualifying home

You must intend to make that home your principal residence within one year

You must be a resident of Canada at the time of the withdrawal and when you buy the home

So yes, you can technically qualify again even if you’ve owned property before. As long as you (and your current spouse or partner) haven’t lived in an owned home in that four-year window, you may still be eligible.

I call this the “fresh start” clause. It’s particularly useful for people who sold a home years ago and have been renting since.

How does the First Home Savings Account define a first-time homebuyer?

The FHSA is the new kid on the block, and honestly, it’s a game-changer. It combines the tax perks of an RRSP and a TFSA, and lets you contribute up to $40,000 toward your first home purchase.

But, like the HBP, it also uses a version of the four-year lookback rule.

Similar to HBP, but tied to ownership and occupancy

To open and use an FHSA:

You must be between 18 and 71 years old and a Canadian resident

You must not have owned or jointly owned, or lived in, a qualifying home in the calendar year before you open the FHSA or during the previous four calendar years

This rule also considers property owned by your spouse or common-law partner that you lived in

The FHSA’s definition of a first-time homebuyer is almost identical to the HBP’s, but there’s one nuance: the timing starts before the account is opened. That means you have to meet the definition at the time you open the FHSA, not just when you use it.

This is crucial. We tell our clients: if you’re even thinking about buying your first home in the next few years, open your FHSA sooner rather than later, even with a minimal contribution, to start that eligibility clock.

How do the definitions compare?

Let’s stack them side by side so you can see where things align, and where they don’t.

Program

Never Owned Anywhere

Four-Year Lookback

Spouse/Partner Ownership Included

Notable restriction

LTT Rebate (ON)

Yes

No

Yes

Ever owned (anywhere) = disqualified

HBP (RRSP)

No

Yes

Yes

4-year rule based on occupancy

FHSA

No

Yes

Yes

4-year rule based on ownership + occupancy

The key takeaway? The LTT rebate is the strictest. HBP and FHSA are more flexible, especially if you’ve taken a break from homeownership or recently separated from a partner who had a home.

Our advice

Don’t assume you are (or aren’t) a first-time buyer until we really look at the details. Each program plays by its own rules, and timing, relationship history, and past ownership all matter.

Here’s what we recommend:

Talk to a mortgage expert early: They can walk you through each of these definitions based on your personal history

Open your FHSA early if there’s any chance you’ll buy in the next few years. You’ll be glad you did

Be honest with yourself (and your partner) about your ownership history, even that vacation property from 15 years ago might count

Don’t leave money on the table. We’ve seen clients qualify for benefits they didn’t know they were entitled to, and others miss out because they made assumptions

Does first-time buyer status matter for mortgage purposes?

Actually, for an insured mortgage, it can matter if you are a first time homebuyer.

Repeat buyers are eligible for a 30-year amortization with mortgage insurance only when purchasing newly built homes.

First-time homebuyers are eligible regardless of whether they are buying a new or resale home.

Repeat buyers purchasing resale (existing) homes are not eligible for a 30-year amortization with mortgage insurance—the maximum remains 25 years in these cases.

Whether you’re buying your very first home or just your first in a while, knowing which programs you qualify for can save you thousands, and make your homeownership journey much smoother.

Ross Taylor is dedicated to empowering Canadians with financial literacy and expertise in housing, credit, and real estate. With over 20 years of experience as a mortgage broker, Ross has helped thousands of Canadians navigate the complexities of home financing and credit management. His passion for education drives him to demystify the mortgage process, ensuring clients make informed decisions. Discover more valuable insights and resources by visiting www.askross.ca/articles

Governor Tiff Macklem says the central bank will examine how its policies affect housing demand and affordability as part of its 2026 framework renewal.

The Bank of Canada will consider how its policies affect housing affordability as part of its next five-year monetary policy framework review.

In a speech delivered Tuesday in Mexico City, Governor Tiff Macklem said the Bank is preparing for its 2026 renewal by examining how monetary policy interacts with a housing market that has become increasingly unaffordable for many Canadians.

“Monetary policy cannot directly increase the supply of housing—that’s an issue for elected governments,” Macklem said. “But, through interest rates, monetary policy does have a direct effect on the demand for housing. And housing is a big part of the consumer price index in Canada, so the cost of housing affects inflation.”

“Therefore, it’s worth examining how monetary policy affects housing sector dynamics, and how best to factor housing affordability into our focus on overall price stability,” he added.

Macklem also hinted the Bank may revisit how it gauges underlying price pressures, suggesting the trim and median core measures could be reviewed. That comes as policymakers face more frequent supply shocks that can distort traditional readings of inflation.

Still, one element won’t change.

“As I said at the start of my remarks, there’s one key question we won’t be asking this time around,” Macklem said. “In our reviews since 1995, we’ve repeatedly asked whether 2% is the right target… Each time, we’ve concluded that targeting 2% inflation is the right framework for us.”

The Bank’s monetary policy framework is reviewed every five years in partnership with the federal government. The last review, completed in 2021, reaffirmed the 2% target and explored alternatives such as price-level targeting and nominal GDP targeting.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.