President Donald Trump has officially confirmed that tariffs on Canadian and Mexican imports will go into effect on March 4, 2025, following his comments earlier this week suggesting a delay.

Trump plans to impose a 25% tariff on imports from Mexico and Canada, while applying a reduced 10% tax on Canadian energy products, including oil and electricity.

In a post on Truth Social, Trump said the decision was driven by ongoing concerns over “unacceptable levels” of drugs entering the U.S. from both countries, with a specific focus on fentanyl flowing through the borders.

“We cannot allow this scourge to continue to harm the USA, and therefore, until it stops, or is seriously limited, the proposed TARIFFS scheduled to go into effect on MARCH FOURTH will, indeed, go into effect, as scheduled,” Trump wrote. “China will likewise be charged an additional 10% Tariff on that date.”

Bank of Canada Governor Tiff Macklem recently warned of the economic fallout Canada could face if the trade conflict intensifies.

“Increased trade friction with the United States is a new reality,” he said, cautioning that such a shock wouldn’t be temporary—it would fundamentally alter Canada’s economic trajectory,” Macklem said.

“The economic consequences of a protracted trade conflict would be severe,” he continued. “If tariffs are long-lasting and broad-based, there won’t be a bounce-back. We may eventually regain our current rate of growth, but the level of output would be permanently lower.”

On Thursday, Mexican President Claudia Sheinbaum expressed optimism, stating that Mexico remains hopeful it can negotiate a deal with the U.S. to avoid the looming tariffs, despite the recent announcement.

Markets are bracing for the impact, as analysts predict that these tariffs could lead to higher costs for U.S. consumers, putting additional strain on the broader economy. This move is expected to heighten market volatility, as traders and analysts weigh the potential ripple effects on global supply chains.

Analysts are watching closely as these moves could signal broader trade tensions, with Trump hinting at further 25% tariffs on the European Union as well.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

Variable mortgage rates are looking increasingly attractive compared to fixed rates, with the potential for significant savings, according to new research from BMO Economics.

With additional Bank of Canada rate cuts expected this year, the bank argues that variable-rate mortgages could offer borrowers more savings over the long run.

“With borrowing costs more likely to fall than rise—and by a lot in a possible trade war—a floating rate mortgage could pay off,” writes senior BMO economist Sal Guatieri.

While current variable mortgage rates are roughly on par with—or slightly higher than—5-year fixed rates, Guatieri notes they’re “unlikely to stay there.”

How variable rates are priced

Unlike fixed mortgage rates, which are influenced by bond yields, variable rates are tied to lenders’ prime lending rates.

These, in turn, follow the Bank of Canada’s overnight policy rate, which currently sits at 3.00%. The current prime rate offered by major lenders is 5.20%, meaning most variable rates are currently priced at a discount off the prime rate.

Most economists expect the Bank of Canada to continue cutting rates this year, in addition to the six consecutive rate cuts the Bank delivered last year. That means lenders’ prime rates should follow suit—bringing down borrowing costs for variable-rate mortgage holders.

Where rates are headed

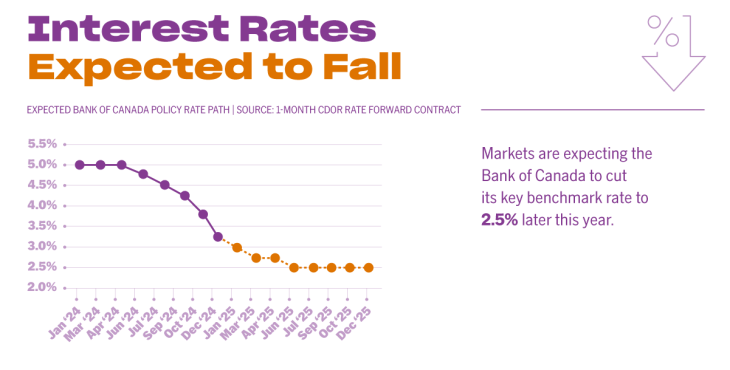

BMO’s latest forecast sees the Bank of Canada’s policy rate falling to 2.50% by later this year, or potentially down to 1.50% in the event of a full-fledged trade war with the U.S. (See full story here). Under the base-case scenario, this would likely push the prime rate below 4.50%, meaning today’s variable-rate borrowers could see meaningful savings.

Other big banks generally share this outlook, with CIBC, National Bank, and TD all expecting the BoC policy rate to drop to 2.25% by year-end, while RBC is even more aggressive, forecasting a fall to 2.00%.

BoC policy rate forecasts from the Big 6 banks

Current Policy Rate:

Policy Rate:

Q1 ’25

Policy Rate:

Q2 ’25

Policy Rate:

Q3 ’25

Policy Rate: Q4 ’25

Policy Rate: Q4 ’26

BMO

3.00%

3.00%

2.75%

2.50%

2.50%*

2.50%

CIBC

3.00%

2.75%

2.25%

2.25%

2.25%

2.25%

NATIONAL BANK

3.00%

2.75%

2.50%

2.25%

2.25%

2.75%

RBC

3.00%

2.75%

2.25%

2.00%

2.00%

SCOTIABANK

3.00%

2.75%

2.75%

2.75%

2.75%

2.75%

TD

3.00%

2.75% (-25bps)

2.25% (-50bps)

2.25% (-25bps)

2.25%

2.25%

* Assumes no U.S. tariffs. Expected policy rate of 1.50% in the event of tariffs. Updated: February 24, 2025

More borrowers are turning to variable rates

Courtesy: Edge Realty Analytics

With variable rates looking more appealing, more borrowers are already reconsidering their mortgage options.

Data from the Bank of Canada shows that as of November, nearly a quarter of new mortgages were variable-rate—up from less than 10% earlier in the year.

Mortgage broker Ron Butler told Canadian Mortgage Trends previously that this trend has only accelerated in recent months, noting that the share of variable mortgages he’s originating has jumped from 7% last year to 40% today.

Why BMO thinks it’s a smart bet

BMO argues that with rate cuts ahead, borrowers choosing variable rates today are positioning themselves for lower payments in the near future.

“We estimate a borrower putting 10% down on a half-million-dollar home financed over 25 years would save an average of 40 bps per year compared with locking in for five years,” he wrote. “That equates to just over $100 per month or more than $6,000 in five years.”

In the event that a trade war with the U.S. “torpedoes the economy,” Guatieri says the savings could be even greater, with variable-rate borrowers saving an additional 29 bps on average over the 5-year term—or an extra $74 per month.”

Another benefit, Guatieri notes, is that that variable-rate borrowers still have the flexibility to lock in if rates unexpectedly start to rise.

While there’s always a degree of uncertainty, Guatieri believes the bigger risk is locking into a fixed rate and missing out on potential savings.

Weighing the risks and alternatives

While BMO’s forecast aligns with market expectations for 50 bps in rate cuts this year, Guatieri acknowledges that there’s no guarantee the Bank of Canada will ease further.

“Should the Bank stand pat on rates, locking in could pay off moderately,” he wrote. “Furthermore, the economy could strengthen materially if a trade war is averted, causing inflation to reheat and the Bank to unwind some rate cuts. In this case, a fixed rate would clearly be the better choice.”

For risk-averse borrowers, a shorter-term fixed rate could be a middle ground.

Three-year fixed rates are currently slightly lower than five-year rates and provide the flexibility to refinance sooner at a potentially lower variable rate. According to BMO, this approach could save borrowers about 20 bps per year over five years compared to locking in for the full five years today.

“While that’s still 20 bps higher than opting for a variable rate today, the extra cost may be worth paying to hedge against potential rate increases,” Guatieri added.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

Canada’s inflation report for January has led to a sharp decline in the chances of the Bank of Canada cutting rates in March.

Canada’s headline inflation rate rose by 1.9% year-over-year in January, a slight increase from December’s 1.8% and in line with expectations.

The increase in headline CPI was largely driven by higher energy prices, notably gasoline (+8.6%) and natural gas (+4.8%).

The Goods and Services Tax (GST) holiday, which ran from mid-December to mid-February, provided some relief. This temporary measure helped reduce prices for food purchased at restaurants (-5.1% y/y), alcoholic beverages (-3.6% y/y), and toys, games, and hobby supplies (-6.8% y/y).

Core inflation measures, which are closely monitored by the Bank of Canada, showed a more mixed picture. CPI excluding food and energy remained stable at 2.2% y/y, but the seasonally adjusted annualized rate of CPI excluding food and energy slowed to 1.6% in January from 4% in December.

However, the Bank of Canada’s preferred core inflation measures, CPI-Trim and CPI-Median, both edged higher to 2.7% y/y, signalling that underlying inflation pressures remain. Moreover, the three-month annualized trend of core inflation has been tracking above 3%, suggesting that core inflation “could continue to rise in the coming months “should continue to grind higher,” noted TD economist James Orlando.

Impact on Bank of Canada rate cut expectations

Following today’s release, market odds of a 25-basis-point rate cut at the Bank of Canada’s March 12 policy meeting dropped to under 30%.

“There is too much underlying inflationary pressure in Canada to warrant an inflation-targeting central bank easing monetary policy further,” wroteScotiabank‘s Derek Holt.

“The state of the job market also does not merit further easing,” he added, referencing January’s higher-than-expected job growth. “Canadian inflation remains too warm for the Bank of Canada to continue easing.”

However, economists remain divided on the Bank of Canada’s next move. Some, like Oxford Economics, still expect the Bank to continue cutting rates in the months ahead.

“The Bank of Canada will be in a bind as it weighs competing concerns over higher prices from the tariffs with the drag on economic growth,” noted Tony Stillo, Director of Canada Economics at Oxford.

“We believe the BoC will look through the temporary price shock and instead focus on the negative implications for the Canadian economy and heightened trade policy uncertainty, leaving it on track to lower the policy rate another 75bps to 2.25% by June 2025,” he added.

TD’s Orlando also underscored the challenge the Bank of Canada faces in balancing competing priorities.

“Does it weigh the downside risks to the economy in the face of U.S. tariffs, or does it focus on recent economic strength and the impact this is having on inflation?” he questioned, while acknowledging that much can change between now and the next BoC policy meeting.

“There is plenty of time between now and March 12, and if the President’s first few weeks are anything to go by, a lot could change before then,” he added.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

After the Bank of Canada’s latest rate reduction 5-year variable mortgage rates are now on par with their fixed-rate counterparts, raising the question: Is now the time to go variable?

With additional Bank of Canada rate cuts expected, variable-rate mortgages are becoming an increasingly attractive option.

But choosing flexibility comes with its challenges—borrowers must weigh potential savings against heightened market volatility and the growing uncertainty surrounding a possible trade war with the U.S.

Ron Butler of Butler Mortgages told Canadian Mortgage Trends that this is the most volatile time he’s seen in the bond market “in forever.”

“It’s literally like 2008, during the Global Financial Crisis, it’s so wild,” he said.

Butler notes that the Canadian 5-year bond yield, which typically leads fixed-mortgage rate pricing, fell from a high of 3.85% in April to 2.64% last week, a significant change in such a short period of time. As a result, following six consecutive Bank of Canada rate cuts, 5-year variable rates are now nearly on par with fixed equivalents.

Clients opting for variable rates in droves

Look past the volatility—and the threat of devastating U.S. tariffs —and variable rates present a compelling case.

Markets are still pricing in at least two more quarter-point Bank of Canada cuts this year, which could push variable mortgage rates down at least another 50 basis points.

Some forecast even more aggressive rate-cut action will be required to counter the ecnoomic shock of a trade war with the U.S.

“I don’t think it’s a stretch to believe that the Bank will reduce its policy rate from its current level of 3.00% down to at least 2% during the current rate cycle,” David Larock of Integrated Mortgage Planners said in a recent blog.

However, he cautions that there is also the risk that rate hikes come back into play should inflationary pressures re-emerge.

“While I expect variable rates to outperform today’s fixed-rate options, I caution anyone choosing a 5-year variable rate today to do so only if they are prepared for a rate rise at some point over their term,” Larock added. “Five years is long enough for the next rate cycle to begin, and for variable rates to rise from wherever they bottom out over the near term.”

Still, it’s a risk more and more borrowers are willing to take. Data from the Bank of Canada shows that as of November, nearly a quarter of new mortgages were variable-rate, up from less than 10% earlier in the year.

Butler says this trend has only accelerated in recent months, noting that the share of variable mortgages he’s originating has surged from 7% last year to 40% now.

“We advise clients to take variable because we now have actual reporting from marketplace analysts that it will go down,” he says. “The fee benefit of variable is a guaranteed penalty amount; you just don’t know what penalty you’re really going to get with fixed.”

Unlike fixed-rate mortgages, which often come with interest rate differential (IRD) penalties that can amount to tens of thousands of dollars, variable-rate mortgages typically carry a much smaller penalty—just three months’ interest—making them a more flexible option for borrowers who may need to break their mortgage early.

Butler argues that if tariffs are imposed, their impact on the mortgage market won’t be immediate, as inflation would primarily rise due to retaliatory counter-tariffs. This lag, he says, could give variable-rate borrowers a window to switch to a fixed rate before higher inflation forces the Bank of Canada to reverse course and hike rates.

“This kind of trade war means that in the beginning, the economy deteriorates, and interest rates go down; it takes nine months or a year for the inflation to really lock into a point where the Bank has to raise rates,” he says. “The inflation spiral takes time. The Bank of Canada will cut long before costs start to increase.”

Tracy Valko of Valko Financial, however, suggests that in such a trade war inflation becomes secondary to more immediate economic indicators, like unemployment. That, she warns, could skyrocket following a tariff announcement as companies brace for impact.

“‘Inflation’ was the word last year; this year I think it will be ‘employment,’ because tariffs will drive unemployment, and people won’t be able to afford housing, which will put a lot of pressure on the government infrastructure,” she says. “I don’t think it will be like inflation, which is a lagging indicator, because businesses will have to adjust quite quickly, and we could see massive unemployment in certain sectors.”

Even Trump’s latest tariff threat on aluminum and steel imports could have devastating impacts on Canadian workers in those industries within days.

Valko adds that high unemployment would potentially drive interest rates down faster—potentially even triggering an emergency rate cut, as National Bank had suggested—to blunt the effects of high tariffs. That potential scenario, Valko says, adds to the variable rate argument, but also adds to the widespread feeling of uncertainty in the market.

“A lot of people are really pessimistic right now on the future; we’ve had clients and homeowners that have had a lot of shocks in the mortgage market and the real estate market, and are not interested in having any more instability,” she says. “People are more educated than they’ve ever been before, so they are really looking at their financing—which is great to see—but people are very cautious, so to take variable, it has to be a very risk-tolerant client.”

Rate options for the more risk-averse borrowers

Valko notes that borrowers wary of economic uncertainty are increasingly choosing shorter-term fixed rates, offering stability without locking in for the long haul.

“Three-year fixed has been probably the most popular because it’s not taking that higher rate for the traditional five-year fixed rate term,” she says. “They’re hoping in three years we’ll see a more normalized and balanced market.”

For more cautious borrowers, hybrid mortgages—which split the loan between fixed and variable rates—are another option and are currently available through most major financial institutions.

“There are some people that are in the middle of that risk tolerance, and if they could put a portion in fixed and a portion in variable—and to be able to adjust it quickly—I think it would be a really good option,” Valko says.

Butler, however, disagrees.

“A hybrid mortgage means you are always half wrong about mortgage rates,” he says. “If the balance of probability clearly indicates variable is the correct short-term answer, take variable and carefully monitor the movement of fixed rates.”

Jared Lindzon is a freelance journalist and public speaker based in Toronto. He is a regular contributor to the Globe & Mail, Fast Company and TIME Magazine, and has been published in The New York Times, Rolling Stone, The Guardian, Fortune Magazine, and many more.

Canada received a temporary reprieve from U.S. tariffs for at least 30 days, but if enacted, BMO warns the Bank of Canada may be forced to cut its policy rate to 1.50% by year-end.

That would be a full 100 basis points (one percentage point) lower than BMO’s current forecast, which expects the Bank of Canada’s rate to hit 2.50% by later this year.

BMO released its updated forecast based on the implementation of U.S. tariffs—20% on most Canadian goods and 10% on oil and gas—which were originally set to take effect today. However, at the eleventh hour, President Trump announced a 30-day delay, extending a similar deal previously made with Mexico.

BMO economist Michael Gregory told Canadian Mortgage Trends that if tariffs do eventually take effect, a more aggressive rate-cutting cycle could be back on the table.

“If tariffs are actually put in place, then -150bps enters the realm of possibilities again,” he said.

This would push Canada-U.S. overnight rate spreads beyond -225 bps, approaching the “all-time extreme” set in 1997, he added.

In the meantime, however, with any action now being postponed, Gregory said the tariffs “have shifted from being an essential certainty to now being a risk.”

BoC policy rate forecasts from the Big 6 banks

Current Policy Rate:

Policy Rate:

Q1 ’25

Policy Rate:

Q2 ’25

Policy Rate:

Q3 ’25

Policy Rate: Q4 ’25

Policy Rate: Q4 ’26

BMO

3.00%

3.00%

2.75%

2.50%

2.50%*

CIBC

3.00%

2.75%

2.75%

2.25%

2.25%

2.25%

National Bank

3.00%

2.75%

2.50%

2.25%

2.25%

2.75%

RBC

3.00%

2.75%

2.25%

2.00%

2.00%

Scotiabank

3.00%

3.00%

3.00%

3.00%

3.00%

3.00%

TD

3.00%

3.00%

2.75%

2.50%

2.25%

2.25%

* Assumes no U.S. tariffs. Expected policy rate of 1.50% in the event of tariffs. Updated: February 4, 2025

Tariffs could justify emergency Bank of Canada rate action

Believing tariffs were imminent, economists at National Bank made said there was a “strong argument” for an emergency or larger-than-usual rate cut.

“To lessen the fallout on Canada’s real economy and to simultaneously buttress financial conditions, we believe there would be a strong argument for an emergency or inter-meeting interest rate cut by the BoC,” they wrote, pointing out that a policy rate of 3% is still in the upper half of the assumed neutral range of 2.25% to 3.25%.

“Note that an emergency action would argue for a larger-than-normal cut of at least 50 bps,” they added.

Beyond this immediate action, the bank also predicted that scheduled cuts in March and April, totalling 25 basis points each, could bring the policy rate down to 2.00% by spring.

Beyond affecting the Bank of Canada’s rate-cutting path, tariffs are expected to put significant pressure on the Canadian dollar and economic growth, with some warning they could push the economy into recession. Experts also highlight the risk of inflationary pressures if tariffs persist.

However, all of this remains speculative and hinges on what happens over the next 30 days.

As part of the deal to delay tariffs, Canada has pledged to step up efforts on border security and the flow of fentanyl by working closely with U.S. officials. This includes expanding its $1.3-billion border protection plan, listing cartels as terrorist organizations, and launching a new cross-border task force.

Canada is also committing an additional $200 million to fight drug trafficking and appointing a fentanyl czar to lead the charge.

Steve Huebl is a graduate of Ryerson University’s School of Journalism and has been with Canadian Mortgage Trends and reporting on the mortgage industry since 2009. His past work experience includes The Toronto Star, The Calgary Herald, the Sarnia Observer and Canadian Economic Press. Born and raised in Toronto, he now calls Montreal home.

Canada Mortgage and Housing Corp. says high housing costs are restricting population mobility in the country, as Canadians are finding that it’s too pricey to buy or rent in cities where they seek jobs.

The federal housing agency said its analysis shows that a one per cent increase of housing prices in a destination city leads to a corresponding one per cent decline in the number of people moving there.

Since 1990, the percentage of households in Canada moving each year — including within municipalities — has dropped from nearly 17.8% to just 10.1% in 2020.

“This trend reflects many factors including population aging and technological changes, but housing costs have a role to play as well,” said CMHC deputy chief economist Aled ab Iorwerth in an online post.

He said the inability to move due to high housing costs is felt by both current workers and those new to the workforce, which limits skill development and reduces the economic growth of major cities.

“When choosing where to live and work, Canadians not only look at the wage increase they might get. They must be realistic about housing costs if they have to move to a new location,” ab Iorwerth wrote.

“And they may give up on opportunities given by a new job that improves their skills and knowledge — and hence the productivity of the country — if they can’t afford to cover the cost of housing after moving.”

Employers in cities with more expensive housing are subsequently forced to offer higher salaries to attract skilled workers to compensate for their cost of living, which raises business expenses and lowers productivity.

The analysis said Toronto, one of the two most expensive major cities in the country to purchase a new home, could boost its population by three per cent if it doubled its housing starts over the next decade.

Ab Iorwerth said that while many attribute the lack of affordability in Toronto and Vancouver to their growing populations, data shows Calgary and Edmonton have remained relatively more affordable despite faster population growth over the past two decades.

“The reason for this is that more housing supply keeps house prices under control relative to income, which in turn attracts people,” he wrote.

“Population growth can be accommodated if there is sufficient housing supply. In contrast, if there is insufficient housing supply then more people arriving in a city will lead to higher house prices limiting growth of the city.”

This report by The Canadian Press was first published Jan. 30, 2025, and found on Canadian Mortgage Trends.